You are entering Acker’s Global Retail Shop. Available stock in the global shop is located in the US and Asia. Local UK stock may be accessed Here or on the homepage UK Stock List.

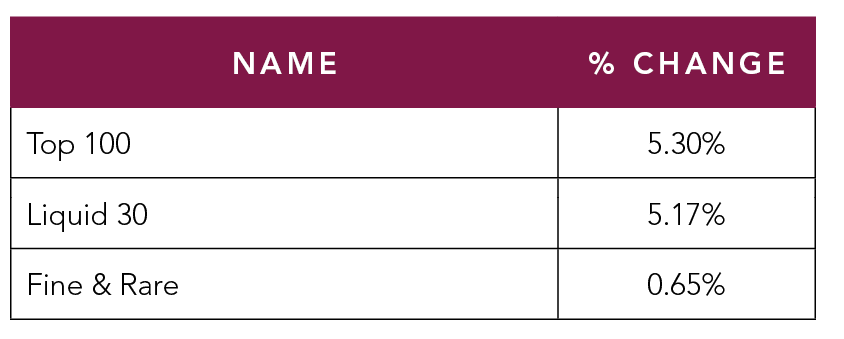

The first half of 2024 demonstrated stability in the fine wine market, characterized by increased volume and a 5% rise in both Acker’s Top 30 and Top 100 indices. The overall Fine & Rare Wine Index saw a modest increase of 0.65%. Acker achieved a 42% global market share, with a 15% increase in volume and nearly 5,000 new world records. Additionally, our global retail and private sales division experienced record volumes during this period.

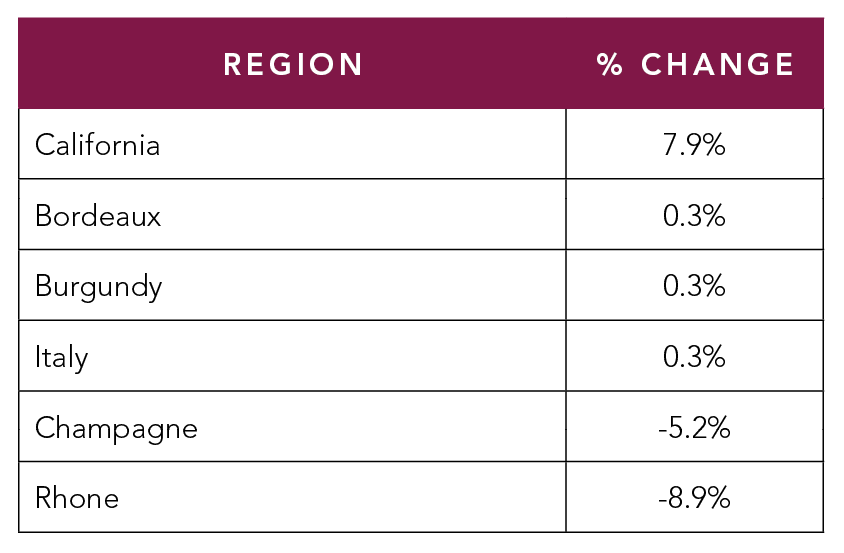

A significant highlight of the first six months was the surge in old Bordeaux wines, with volumes of pre-1975 vintages rising over 200%. Demand for these wines remains exceptionally strong, with our historic Bordeaux indices dominating the top five indices of 2024. Burgundy showed healthy market stability, with 83% of the top world records set by Burgundy wines. Our California index was the top regional performer, rebounding by 7.9%, while Champagne and Rhone

experienced softer prices.

Young Bordeaux continued to face distribution challenges from 2023, although supply pressure is significantly easing.

The top overall producers from the two largest volume regions were Chateau Lafite and Chateau Palmer from Bordeaux, and Pierre-Yves Colin-Morey and Comte Liger-Belair from Burgundy.

top 5 indices overall

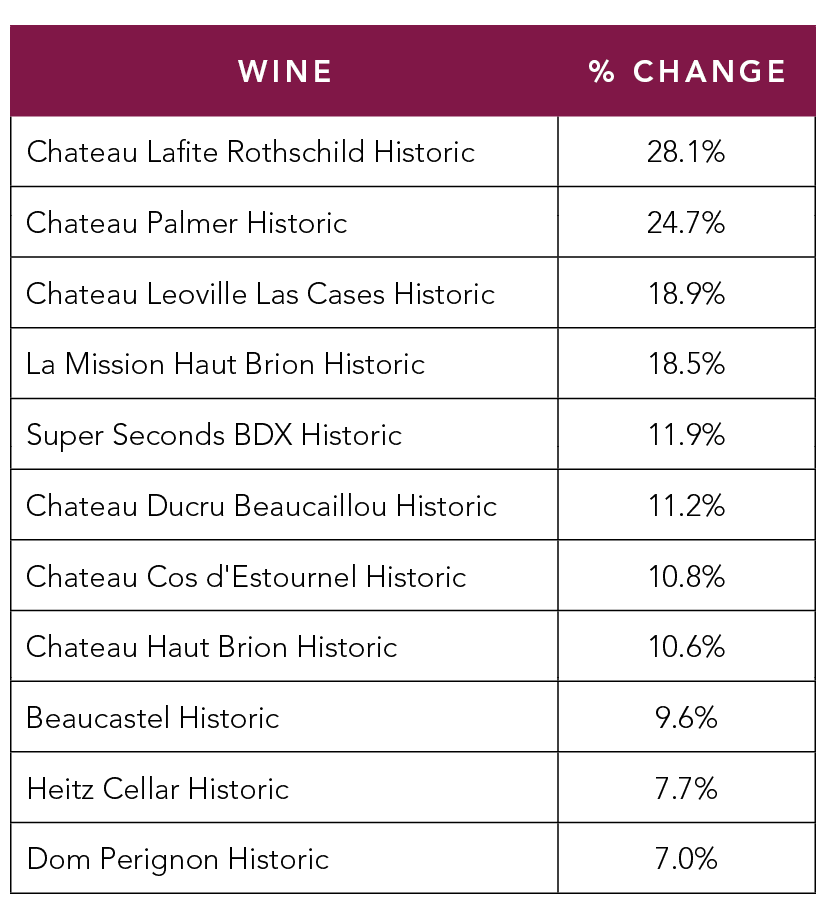

top 10 historic indices*

*Historic Indices are comprised of a selection of the most traded wines from a given producer before the year 2000. The selection of wines and the index’s pricing scale are static as of the index’s creation date.

Overall, global demand and distribution of buyers were much healthier in 2024, although the Asia market continued to be impacted by the Chinese economy. In a hopeful sign, activity from the other Greater Asia countries has stabilized and begun to increase.

The strong regional performance of the California Index was driven by wines of the 1990’s and 1980’s, specifically Dunn, Heitz Cellar, Screaming Eagle and Shafer, all with gains over 10%.

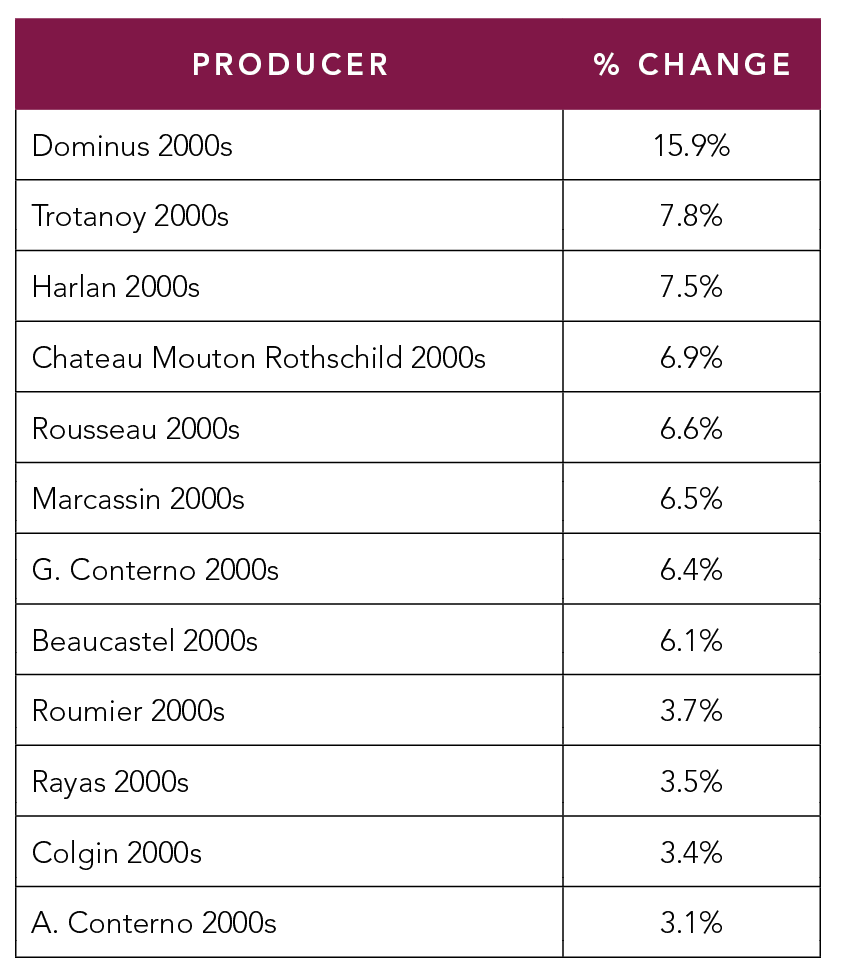

The demand for wines of the 2000-2010 period remained strong across most of the regions as indicated by the top 2000’s indices.

regional performance

Acker Indices

top 2000s indices*

*2000s Indices are comprised of a selection of the most traded wines from a given producer between the year 2000 and 2020. The selection of wines and index’s pricing scale are static as of the index’s creation date.

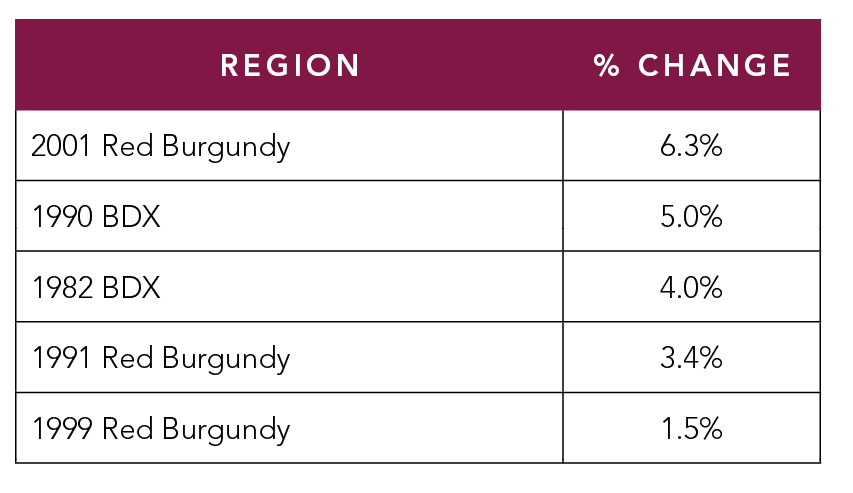

top vintage performers

The top vintage performers were split between Burgundy and Bordeaux.

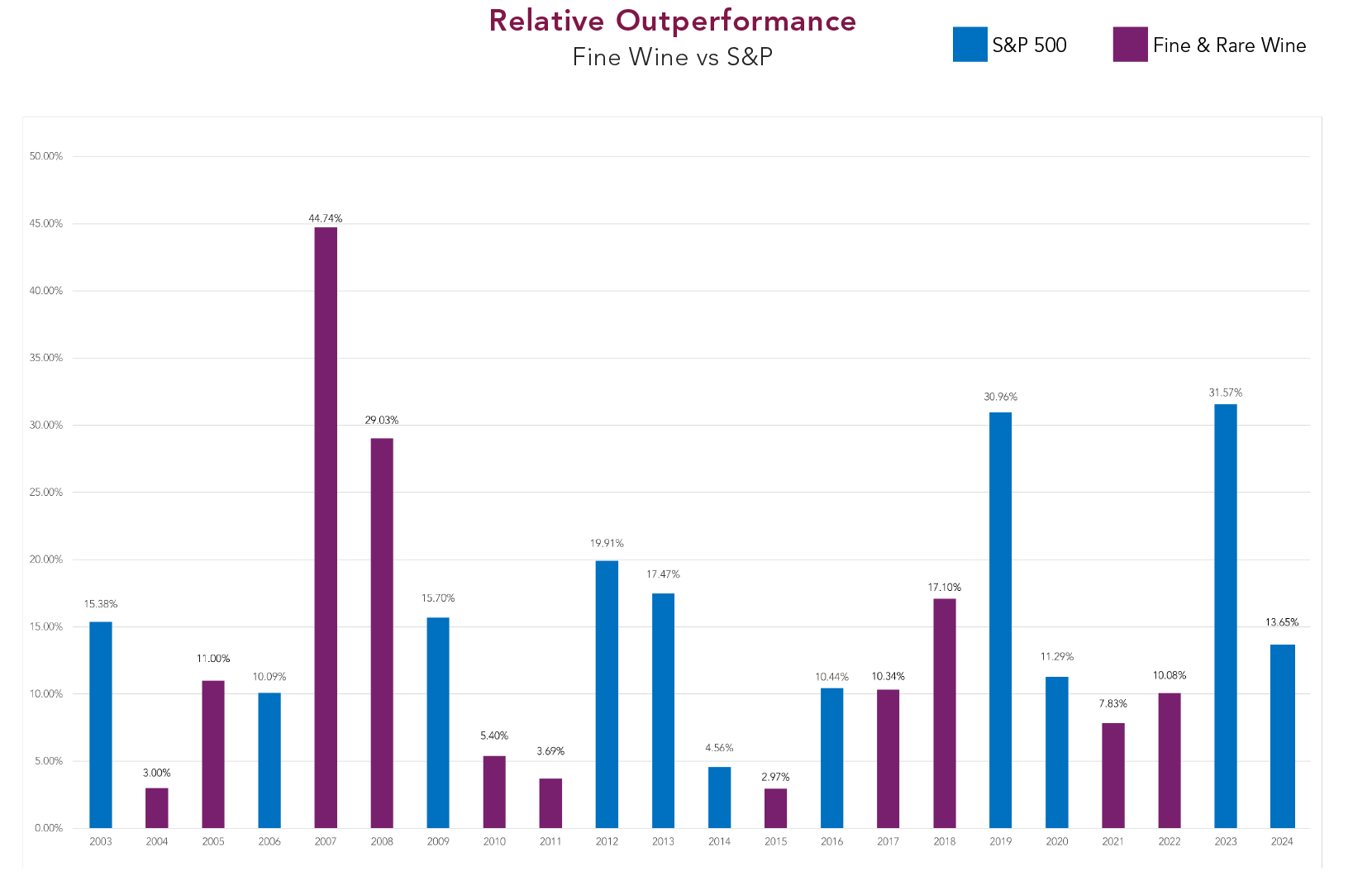

As highlighted in our annual report, the outperformance of stocks relative to wine in 2023 was the largest ever recorded, and this trend continued, albeit at a much slower pace. It is important to note that most of the performance of stock

indices has been dominated by seven specific stocks, and this narrow breadth of performance is distorting historical

comparisons.

Summary

The fine wine market stabilized in the first half of 2024, indicating a promising and dynamic market for the latter half of the year. Historically, the wine market has shown no statistical evidence of being influenced by elections. We believe the

stabilization observed in the first half, along with several positive indicators such as increases in number, breadth and

geographical distribution of buyers has set the stage for overall price increases and a healthy market in the second half

of 2024. Wishing everyone an enjoyable summer.

Sign up for Acker exclusive offers, access to amazing

wine events & world-class wine content!

Please note there will be a credit card usage fee of two percent (2%) on the total auction purchase price up to the credit card payment limit of USD$15,000, HKD$150,000, or SGD$20,000 for live auctions, and on the total amount charged on internet auctions (except where prohibited by applicable law).

Acker uses cookies to improve your experience on our website. Some cookies are essential to make our website work. We track website preferences, provide product recommendations, and record anonymized data about your site visit with cookies. To learn more about how we use cookies, see our Privacy Policy.